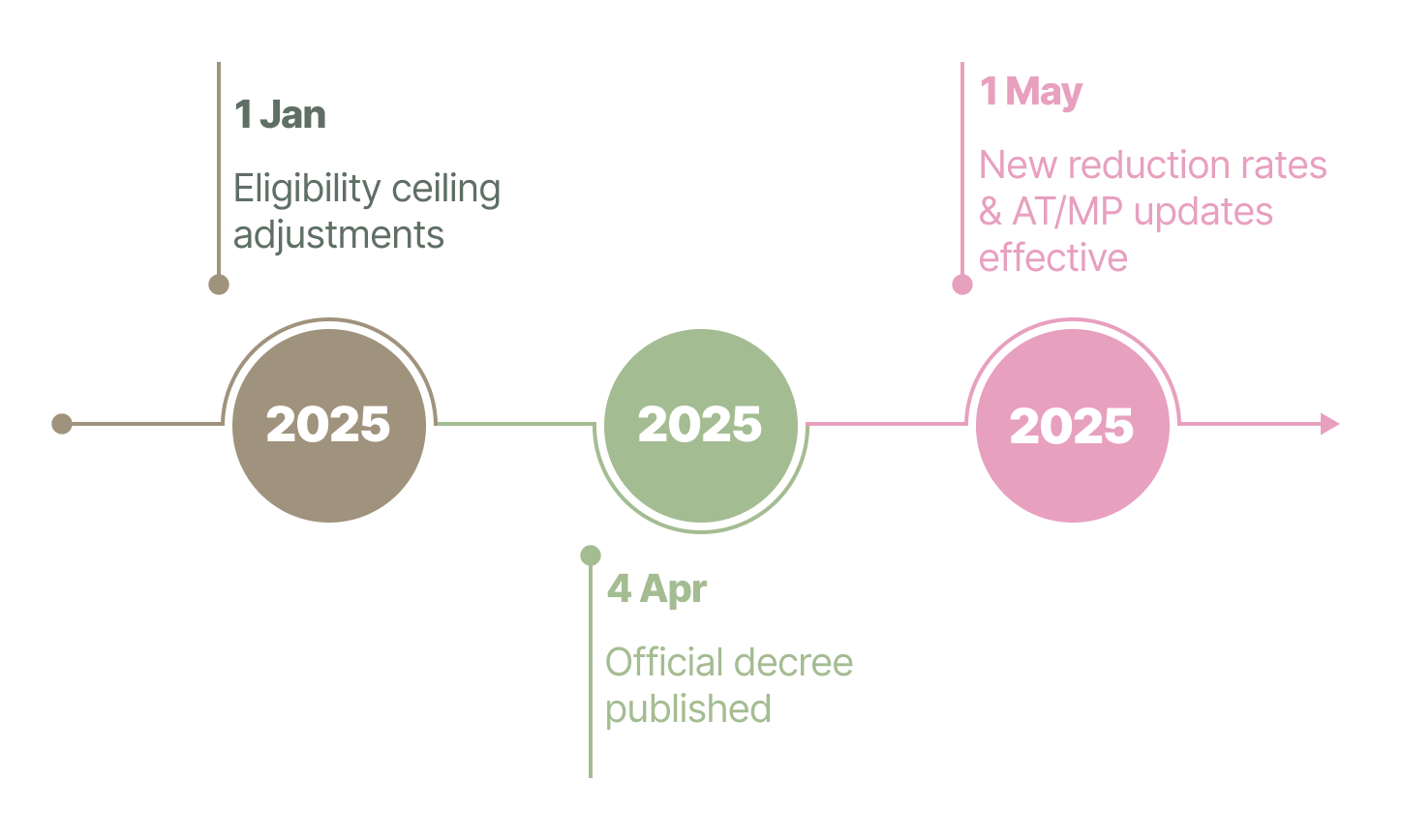

From May 2025, a series of important updates will take effect regarding employer social contributions in France. Introduced by the decree of 4 April 2025, these changes impact contribution rates related to payroll, unemployment insurance, and overtime deductions. Employers and HR teams should take note of the new rates to ensure accurate payroll compliance.

Key 2025 milestones for employer contribution updates.

General Reduction in Employer Contributions

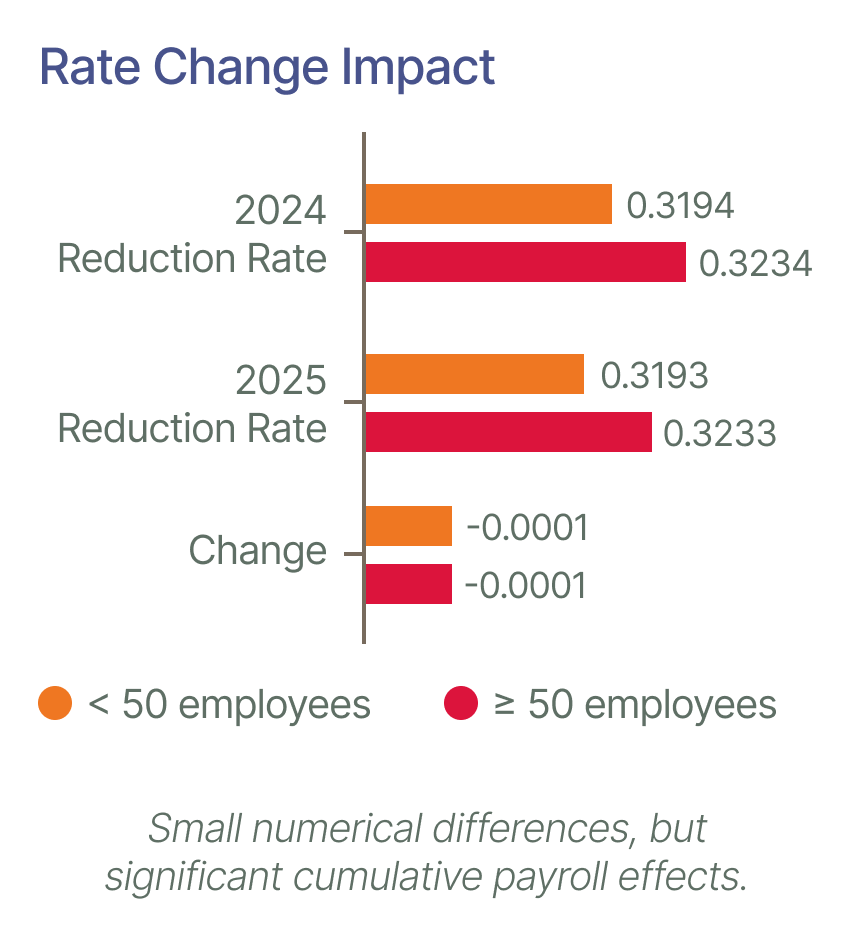

Effective 1 May 2025, the general reduction in employer social contributions — often referred to as the T-value — will be slightly adjusted. The updated reduction rates are:

- 0.3193 for businesses with fewer than 50 employees (previously 0.3194)

- 0.3233 for businesses with 50 employees or more (previously 0.3234)

Although minor, these adjustments affect how payroll teams calculate the reduction coefficient. The formula remains as follows:

[Reduction rate / 0.6] × [(1.6 × gross annual minimum wage / gross annual remuneration) – 1].

The 2025 Budget Law also confirms that the value-sharing bonus (prime de partage de la valeur) is now included in the base for calculating this reduction.

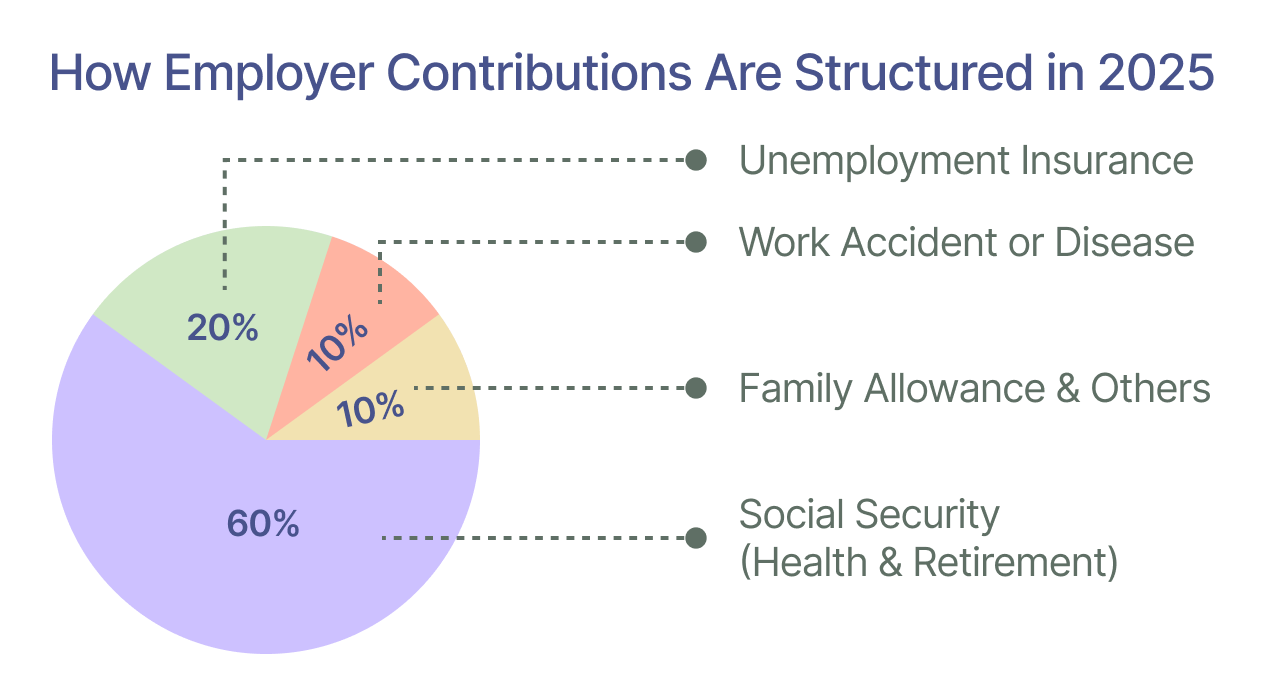

Accident-at-Work and Occupational Disease Contributions

The Accident-at-Work and Occupational Disease (AT/MP) contribution rate will also evolve on 1 May 2025. Employers can view their specific rate in their online AT/MP account.

Until 30 April 2025, the 2024 rates remain applicable. From May onward, the pooled share of the AT/MP rate, used to calculate the T-value, will increase from 0.46% to 0.50%, setting a new minimum contribution threshold.

Unemployment Insurance Contributions

The unemployment insurance contribution rate for employers will slightly decrease from 4.05% to 4.00% as of 1 May 2025. This change results from an adjustment in the unemployment insurance bonus-malus system under the new insurance convention.

The rate continues to operate within defined limits, meaning it cannot fall below 2.95% or exceed 5.00%.

Flat-Rate Deduction for Overtime

A notable new measure introduced by the April 4 decree is a flat-rate deduction of €0.50 per overtime hour on employer social contributions. This incentive is designed for companies with 50 to 249 employees, offering moderate relief for mid-sized employers managing fluctuating workloads.

Revised Thresholds for Sickness and Family Allowance Reductions

Under the 2025 Social Security Financing Act, eligibility thresholds for contribution reductions on sickness insurance and family allowances have been updated. These apply to employment periods beginning on or after 1 January 2025:

| Contribution Type | Eligibility Ceiling | Reduction Rate |

|---|---|---|

| Sickness Insurance | 2.25 × minimum wage (down from 2.5) | 7% |

| Family Allowances | 3.3 × minimum wage (down from 3.5) | 3.45% |

The minimum wage (Smic) used for these calculations is the rate effective 1 January 2025, as confirmed by the April 7 application order.

Preparing for Compliance in 2025

While many of these adjustments are incremental, they collectively impact employer contribution calculations and payroll management. HR and finance teams should review their payroll systems, update parameters, and verify that contribution rates reflect the latest regulations from May 2025 onward.

Maintaining compliance not only avoids administrative errors but also ensures that businesses apply every eligible reduction accurately, supporting better cost management and financial transparency in 2025.

Easy to start,

intuitive to use