The IR56 forms are official documents designated by the Hong Kong Inland Revenue Department (IRD), used by employers to report employee income. These forms are part of a series designed to cover different scenarios such as employment, termination, departure from Hong Kong, and payments to non-employees.

Common Types of IR56 Forms

| Form | Usage | Submission Timing |

|---|---|---|

| IR56B | For current employees | Submitted during the tax season in April, reporting employee income for the previous fiscal year (April 1 – March 31) |

| IR56E | For new hires | Submitted within 3 months of employment to notify IRD of the new hire |

| IR56F | For employees resigning (not leaving HK) | Submitted when an employee permanently leaves the company but stays in Hong Kong |

| IR56G | For employees leaving Hong Kong | Submitted when an employee is terminating employment and departing from Hong Kong |

| IR56M | For non-employees | Used to report payments made to freelancers, consultants, directors, etc. who are not considered employees |

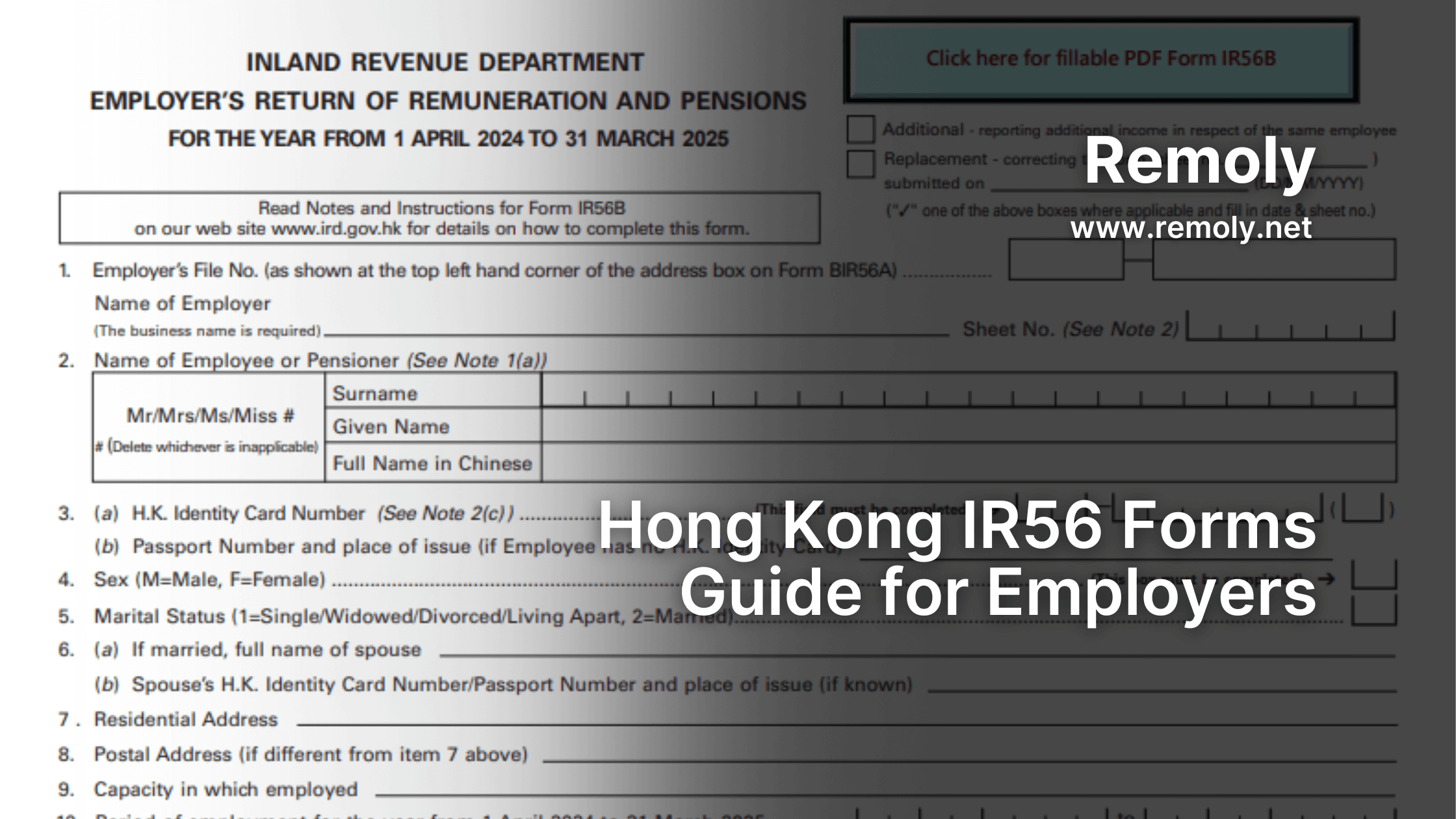

Annual Filing: IR56B + Employer’s Return (BIR56A)

Each April, the IRD sends out:

- BIR56A – the main Employer’s Return form

- IR56B – submitted for each employee (current or past) to report their income (excluding MPF contributions)

Employers must submit the completed forms within one month of receiving the notification, using one of the following methods:

- Print and mail paper forms

- Use the eTAX online platform

- Use the IRD’s IR56 Forms Preparation Tool

Information Required on IR56B

- Employee name and HKID/passport number

- Job title and employment period

- Taxable income including salary, bonuses, and allowances

- Employer’s MPF/retirement fund contributions (excluding voluntary contributions)

- Employment status (currently employed or not)

FAQs

Q1: Do I need to file IR56 forms for non-Hong Kong residents?

A: Yes. If they were employed and received income in Hong Kong, they must be reported regardless of residency status.

Q2: Can I submit IR56F/G a few months after the employee leaves?

A: No. IR56F or IR56G must be submitted at least one month before the employee resigns or leaves Hong Kong. Late submission may result in penalties.

Q3: Are freelancers also covered by the IR56 forms?

A: Yes. If a company pays fees to freelancers, consultants, or directors, IR56M must be filed to report those payments.

Easy to start,

intuitive to use